Weekly Grain Market Recap

Posted: Aug. 12, 2023, 6:50 a.m.

Grain Market Recap:

Each of the major grain contracts closed lower today, and this week, despite a number of potentially bullish anecdotes in today’s WASDE report. It was an abnormal trade across the grain sector this week. In last night’s session, December corn traded in a 2 cent range - that hasn’t happened in years. Meanwhile, the market continued to discount supply-side risk headlines stemming from the Ukraine-Russia conflict when Russia struck ports along the Danube River very close to Romania on Thursday (NATO ally).

Corn:

The December corn contract has endured a myriad of bearish headlines over the last three weeks. Even with lower-than-expected yields in today’s WASDE report, the contract settled 9 cents lower at 487-2. Today’s loss represented an overwhelming majority of the week’s loss, as the contract was only 10 cents lower for the week after opening at 497-6. Usually, when such significant consolidation occurs, it serves as a powder-keg. This was also the case last month as the contract rallied significantly, and subsequently sold off within the 2 weeks following the July 12th WASDE report. In today’s report, new crop corn yield estimates were reported below market expectations coming in at 175.1 BPA (175.5 BPA average estimate, 177.5 BPA last month). The most significant contributory factor in today’s selloff was likely higher-than-expected ending stocks for both old and new crop corn. Old crop (2022/23) corn carry out was reported at 1.457 bil bu (1.410 bil bu expected), while new crop corn stocks were 2.202 bil bu (2.168 bil bu expected). Bottom line is that the market can only move in a singular direction for so long, and the degree of market consolidation observed this week is evidence of a breakout. Has the December corn contract endured enough bearish headlines and headwinds to make a move higher? We managed to bounce off of our 3-star support level in Friday’s trade (480-483), but the December corn contract has to work its way back to the 502-506-4 pivot pocket if we’re going to test resistance. Managed money has compounded its bearish bias, but a net-short position of 33,053 contracts is hardly significant. Broken down, that’s 213,127 short positions and 180,074 long contracts.

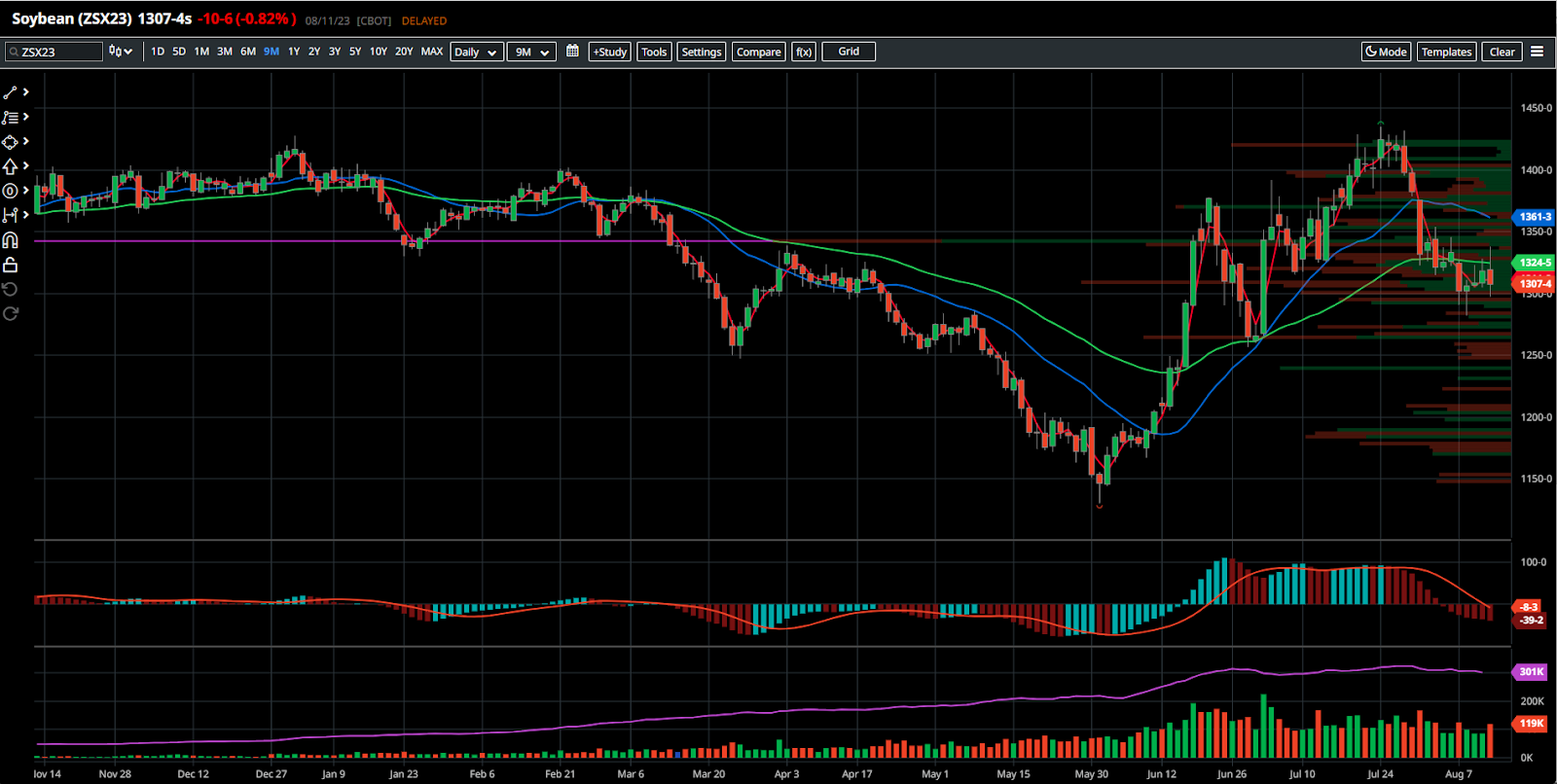

Soybeans:

November soybeans remain the most fundamentally well supported component of the grain complex. Despite both new crop yields and ending stocks estimates coming in below the trade’s expectations, the contract managed to shed 10-6 cents today to settle the week at 1307-4. For the week, November beans were down 25-6 cents. New crop soybean yields were reported at 50.9 BPA (51.3 average trade estimate), while ending stocks were reported at 245 mil bu (267 mil bu expected). Demand cuts for corn, soybeans, and wheat seemed to be the prevailing narrative that the market latched on to. Soybean exports were slashed by 25 mil bus to 1,825 mil bus (compared to 1,850 last month). Even though export sales have picked up over the last three weeks, USDA felt compelled to adjust their estimates lower as new crop commitments are lagging where commitments were at the same time last year. As in corn, it would not be all that surprising for soybean prices to make a bounce back next week - especially if we see another flurry of flash sales. Managed money maintains their bullish bets with a modest net-long position of 62,977 contracts (102,379 long positions and 39,402 short positions), and that is certainly a position that could be built upon.

Wheat:

Price action on the September wheat contract was mostly disappointing this week. The contract closed 11 cents lower today, settling at 626-6 for the week. We spent the entire week ranging between our 4-star support pocket between 622-632, and if we see a pop in either corn or soybeans next week, the lower boundary of that support pocket may be the launch pad. The majority of the figures in today’s WASDE report were in line with the trade’s expectations. All wheat production was reported at 1.734 bil bu, which mirrored the 1.739 bil bu pre-report average estimate. Like corn and beans, demand cuts remained the dominant concern, and that added to wheat’s ending stocks estimates - reported at 615 mil bu (598 mil bu expected). Funds remain mostly pessimistic on the outlook for wheat, holding a net-short position of 62,145 contracts. Broken down, that;s just 57,412 long positions compared to 119,557 short positions. Hopefully, wheat can ride a wave back into our 669-673 pivot pocket next week.

Sign up for a 14-day, no-obligation free trial of our proprietary research with actionable ideas!

Free Trial

Start Trading with Blue Line Futures

Subscribe to our YouTube Channel

Email info@Bluelinefutures.com or call 312-278-0500 with any questions -- our trade desk is here to help with anything on the board!

Futures trading involves substantial risk of loss and may not be suitable for all investors. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. Trading advice is based on information taken from trade and statistical services and other sources Blue Line Futures, LLC believes are reliable. We do not guarantee that such information is accurate or complete and it should not be relied upon as such. Trading advice reflects our good faith judgment at a specific time and is subject to change without notice. There is no guarantee that the advice we give will result in profitable trades. All trading decisions will be made by the account holder. Past performance is not necessarily indicative of future results.

Blue Line Futures is a member of NFA and is subject to NFA’s regulatory oversight and examinations. However, you should be aware that the NFA does not have regulatory oversight authority over underlying or spot virtual currency products or transactions or virtual currency exchanges, custodians or markets. Therefore, carefully consider whether such trading is suitable for you considering your financial condition.

With Cyber-attacks on the rise, attacking firms in the healthcare, financial, energy and other state and global sectors, Blue Line Futures wants you to be safe! Blue Line Futures will never contact you via a third party application. Blue Line Futures employees use only firm authorized email addresses and phone numbers. If you are contacted by any person and want to confirm identity please reach out to us at info@bluelinefutures.com or call us at 312- 278-0500

Like this post? Share it below:

Back to Insights

In case you haven't already, you can sign up for a complimentary 2-week trial of our complete research packet, Blue Line Express.

Free Trial